Here’s a scenario that plays out thousands of times every year.

Someone gets a job offer. They’re excited. The salary is $85,000. That sounds like a lot of money. They accept. They tell their friends. Everyone congratulates them.

Then they get their first paycheck. And reality hits.

The deposit is maybe $4,500 for the month. Not the $7,000 they were imagining. They do the math. Rent is $2,000. Student loans are $500. Car payment is $400. Groceries, utilities, phone, internet. Suddenly that $85,000 doesn’t feel so big.

The problem wasn’t the offer. The problem was not understanding the gap between what a company pays and what a person actually keeps.

Why the Number on Paper Lies to You

Every job offer comes with a number. That number is your gross salary. It’s what the company budgets for your position. It’s what goes in the contract. It’s what you tell people when they ask what you make.

But it’s not what you spend. It’s not what you save. It’s not what you live on.

What you live on is your net pay. Your take-home. What’s left after federal taxes, state taxes, Social Security, Medicare, health insurance, retirement contributions, and everything else has been taken out.

And here’s the thing nobody tells you: the gap between gross and net can be huge. Depending on where you live and your personal situation, you might keep anywhere from 65% to 85% of your gross salary. That $85,000 job could mean $55,000 in your pocket. Or $72,000. It depends.

The Geography of Your Paycheck

If you live in the United States, where you live matters enormously.

Federal taxes are the same no matter what state you’re in. Progressive brackets from 10% to 37%. Standard deduction of about $15,000 for single filers. Everyone deals with the same federal system.

State taxes are where things get wild.

Texas, Florida, Nevada, Washington, Wyoming, South Dakota, Tennessee, and Alaska have no state income tax at all. Zero. If you live there, that’s thousands of dollars in your pocket every year that someone in California or New York pays in state taxes.

California’s top rate is over 13%. New York’s is over 10%. New Jersey, Oregon, Minnesota, all high. The difference between a job in Austin and a job in San Francisco isn’t just cost of living. It’s also thousands of dollars in state taxes.

Local taxes exist in some places. New York City has its own tax. So does Philadelphia. So do many other cities. Another chunk out of your paycheck.

The Deductions You Actually Control

Here’s something people don’t think about enough: some of what comes out of your paycheck is within your control.

401(k) contributions come out before taxes. Every dollar you put in reduces your taxable income. If you’re in the 22% bracket, $1,000 in your 401(k) saves you $220 in federal taxes right now. Plus state taxes. Plus it’s growing for retirement. That’s free money.

Health insurance premiums are usually pre-tax. That means the money you pay for coverage doesn’t get taxed. Another small boost to your effective take-home.

Health Savings Accounts are even better if you have a high-deductible plan. Pre-tax going in. Tax-free growth. Tax-free withdrawals for medical expenses. It’s the only account that’s triple tax-advantaged.

Flexible Spending Accounts let you set aside pre-tax money for medical or dependent care expenses. Use it or lose it, but if you have predictable costs, it’s pure savings.

The choices you make about these things can shift your take-home payby hundreds of dollars per month.

What You Can’t Control

Some things are just fixed.

Social Security takes 6.2% of your wages up to about $168,000. After that, you stop paying. But if you’re under that limit, it’s coming out every paycheck.

Medicare takes 1.45% of everything. No cap. If you’re a high earner, there’s an extra 0.9% on income over $200,000.

Federal tax brackets are what they are. You can plan around them, but you can’t change them.

State tax brackets are what they are. You can move to a different state, but you can’t change the rates where you live.

Why Comparing Job Offers Is Harder Than It Looks

Imagine you have two offers.

Job A is in Austin, Texas. Salary $90,000. No state income tax. Lower cost of living.

Job B is in San Francisco, California. Salary $110,000. High state income tax. Much higher cost of living.

Which one leaves you with more money at the end of the month?

You can’t answer that without doing the math. The $110,000 sounds bigger. But after California taxes, after Bay Area rent, you might actually have less disposable income than the $90,000 job in Austin.

This happens constantly. People chase bigger numbers without understanding what those numbers actually mean where they’ll be living.

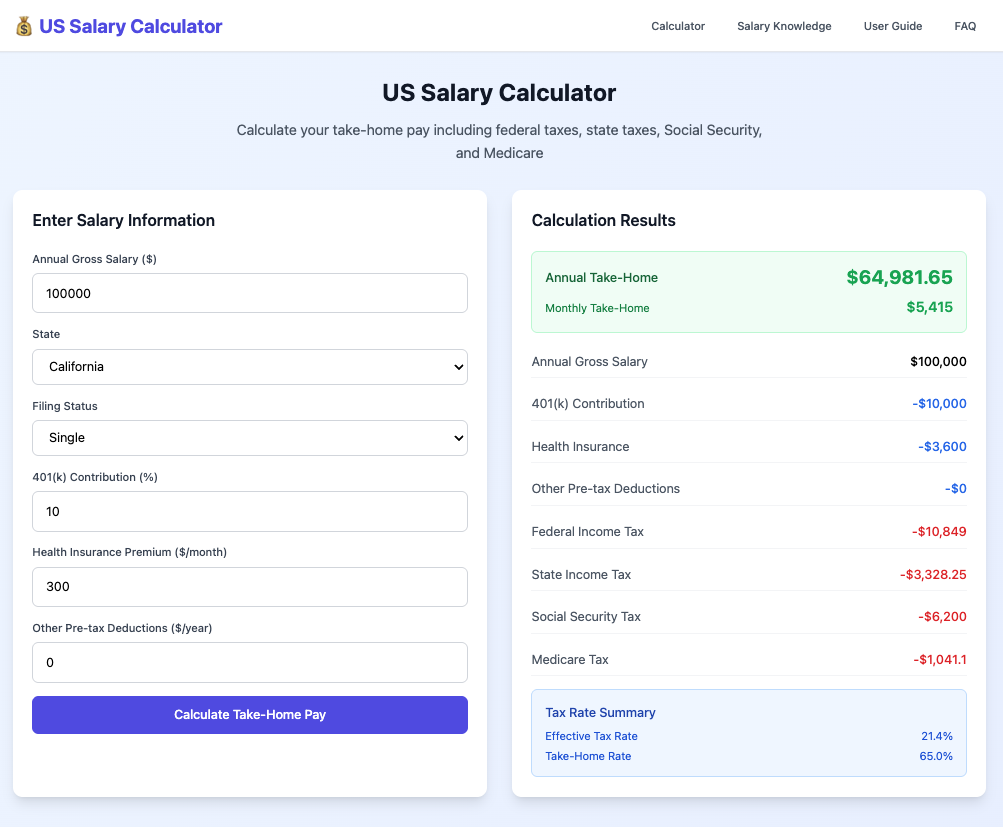

A good US salary calculator shows you the real picture. Not just gross vs net, but month by month, deduction by deduction. You can see exactly what you’ll have for rent, for savings, for everything else.

What You Can Learn From Your Own Numbers

Once you start looking closely at your paycheck, patterns emerge.

You might realize you’re contributing too much to your 401(k) and can’t afford your rent. Or too little and missing out on tax savings.

You might realize your health insurance plan is costing you more than it should based on your actual medical needs.

You might realize that the raise you just got pushed you into a new tax bracket, and you need to adjust your withholding.

You might realize that moving to a different state for a job isn’t worth it once you account for taxes and cost of living.

These aren’t small things. They add up to thousands of dollars every year.

The Moment It Actually Matters

Most of the time, you don’t think about any of this. You get paid, you pay bills, you move on.

But then a moment comes when you have a decision to make. A new job. A move to another city. A promotion with a big raise. A chance to go remote and live somewhere cheaper.

In that moment, guessing isn’t good enough. You need to know.

What will I actually take home each month?

How much will state taxes cost me?

Is this raise worth moving for?

Can I afford to buy a house on this salary?

A good tool answers those questions. Not with estimates, but with numbers. Not based on averages, but based on your specific situation.